Financial Access and Inequality

Poor access to banks and easy access to payday lenders prevent many communities from achieving financial security

For more stories like this, follow my Substack at American Inequality

Americans cannot function without access to banking services. However, 1 in 18 US households (7.1 million families) was unbanked in 2020 according to the FDIC. This inequality persists because the country’s 168,450 bank branches are physically inaccessible in hundreds of US counties. Households lacking banking options often turn to alternative financial services, like payday lending. Families then get caught in endless debt traps, which exacerbate income and wealth inequality. This article looks at the regions in the US that have the worst access to banking services, and the corresponding fallout that happens when those regions turn to payday lenders.

Being unbanked can be expensive, as high-fees can accrue quickly for families already living on low incomes. For example, families without a regional bank will often deposit their paychecks directly onto prepaid debit cards. However, this unavoidable decision will cost those families $197 in fees each year. While half of the unbanked population say they intentionally choose to be unbanked, the other half is forced to bear these types of costs and more.

Donaldo Espinoza is one of these unbanked Americans who struggles with financial access. Donaldo has no access to a bank and so he has been literally storing cash under his mattress for years. Donaldo remains unbanked because his bank won’t accept his ID. He is from Honduras, is a 54-year old construction worker living in the Bronx and has been working for months to open a bank account. When he took the long train ride to Lower Manhattan, Donaldo was denied an account because he didn’t have the right form of ID. In the end, Donaldo had to miss a day of work only to spend $70 to renew his Honduran passport, which he used to open an account at the bank.

The states across the South of the United States have the most unbanked people. This is particularly acute in Jackson, Mississippi. 17.1% of the 166,000 residents do not have a bank account, according to the FDIC, which is more than triple the national average. This has increased by 5% over the last 5 years. Median income in Jackson is $37,000 and the county is 82% Black.

Low-income populations have much lower access to banks. According to the Federal Reserve, 1% of those with incomes over $40,000 are unbanked, versus 14% of those with incomes under $40,000.

We see this trend also hold up across demographics. 17% of Black people and 14% of Latinx people are unbanked, versus 3% of White people. As a result, the loss of financial access means that “Black and Hispanic people are spending 50–100% more per month for basic banking services, which, over a lifetime, can cost $40,000 in fees,” according to Wole Coaxum, founder and CEO of MoCaFi.

According to a report from the National Community Reinvestment Coalition, banking deserts disproportionately impact racial minority populations. 25% of all rural bank closures between 2008 and 2016 occurred in majority-minority census tracts, even though only 10% of all census tracts are majority-minority.

Payday Lending and Debt Traps

Payday lending and banking deserts go hand-in-hand. Low-income communities can often get caught in banking-access traps where the lack of banks means that these communities turn to alternative financial services. These services tend to charge higher fees, which in turn makes it harder to save, which makes it harder to reach the minimums required to open up a bank account, which in turn keeps community members entrenched in these costly alternative services.

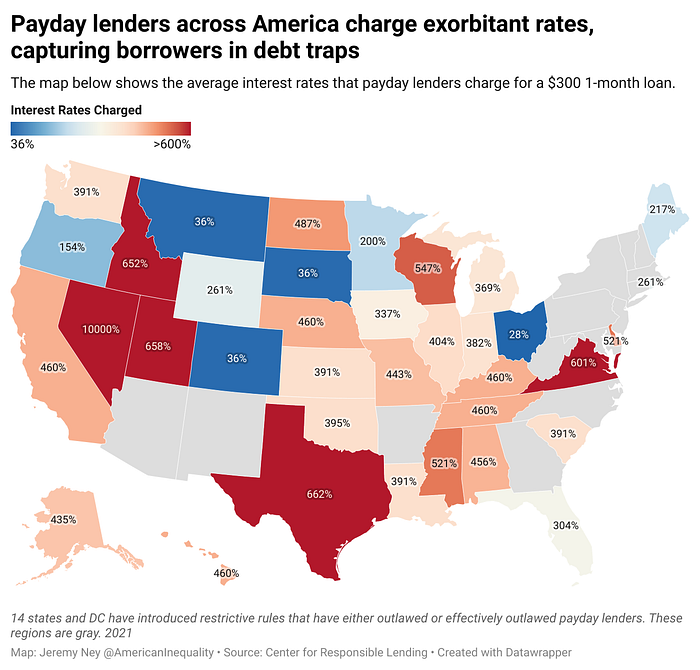

The average payday loan interest rate is 391%, which is absolutely crippling for borrowers who have no other options. The way this plays out for the 12 million Americans who rely on payday loans works like this — a borrower will go to a payday lender and get a $300 loan, which is the typical amount. With a 391% interest rate, that borrower will have to figure out how to pay back the $300 principal, but also $1,173 in interest. The US minimum wage will earn you $1,160 in one month, so even if you spent every cent of every paycheck paying back your loan, you’d still be unable to cover the interest and forget the principal.

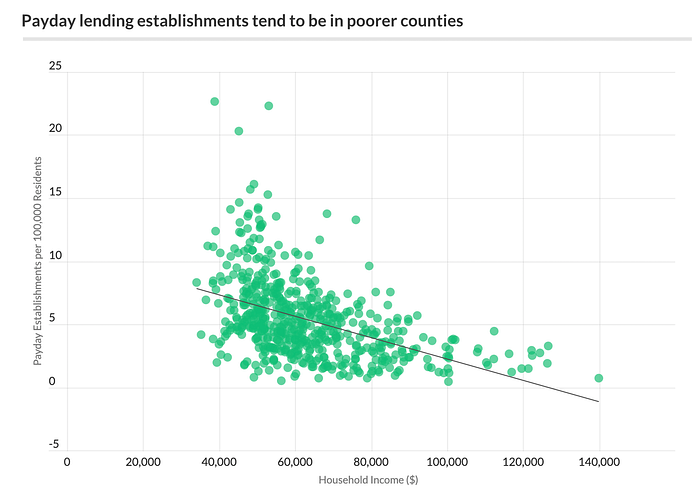

Payday lending is correlated with poorer communities and Black communities. Data from 3,143 US counties shows that counties with lower household incomes tend to have higher rates of payday lending establishments. This is because payday lenders know that low-income communities are often underbanked (see Fed data above) and have no other option but to turn to alternative financial services. This isn’t the case in wealthier regions. We also see a correlation between the racial composition of a county and how many payday lenders it has. Payday lenders appear more frequently in communities that have a higher percentage of Black residents, which may mean these communities are more likely to get caught in debt traps.

Payday lending may be the only option for the 40% of Americans who can’t find $400 in the event of an emergency. For those who can’t pay off the $1,473 in debt, they will often rollover that debt, getting caught in an endless debt trap with payday lenders, who legally have access to your bank account and can draw down funds when they want.

Payday lenders make almost all their money from debt traps. The CFPB found that payday lenders make 75% of their profits from borrowers who took out 10+ payday loans in a 12-month period. They also found that 4 out of 5 payday borrowers renew their loans before their next paycheck, since they are still unable to make ends meet when the principal and interest payments come due. 1 in 5 renewed 7+ times, which often means that borrowers accumulate fees that typically exceed the amount originally borrowed (i.e. I borrowed $300 in week 1, but in week 8 I’ve accumulated $400+ in fees).

Just like banking deserts, payday lenders are more common in the South. The top 10 counties with the highest number of payday lending establishments per 100,000 residents are all in the South. Mississippi has two of the top 10 counties, while Louisiana has five of the top 10 counties.

The Path Forward

We can improve access to financial services through public, private, and novel systems. First, we can improve legislation that has been stalled for decades to encourage more community investment in banking services; second, we can improve digital access to banking services; and third, we can improve the overall system of banking services by not penalizing people for poor banking choices made in the past that might not have been their fault.

First, Enhance the Community Reinvestment Act — The Community Reinvestment Act (CRA) is meant to ensure that banks invest in underserved communities. The CRA was first turned into law in 1977, but has not been updated since 1995. The 3 organizations in charge of enforcing the CRA — the Federal Reserve, the FDIC, and the OCC — are working to modernize the CRA, but are in disagreement about how to actually do this. In 2008, the FDIC proposed giving banks higher CRA grades if they provided safe alternatives to payday loans, but this was never incorporated into the actual legislation. This would be a strong step towards reducing reliance on payday lenders and helping borrowers avoid the debt trap. Additionally, the CRA should continue to expand how it defines “Assessment Areas” to support communities that may not have a physical bank branch present.

Second, Increase Access to Digital Banking — Bank branches are no longer essential for banking. 71% of Americans bank online now and mobile banking has accelerated particularly during the COVID-19 pandemic, with increases of 200% in the early days of lockdowns. While generational differences exist, banks can do more to encourage people to bank online through two major steps. First, people need to be able to get online in order to bank online and so we need to improve internet access. 21 million Americans do not have access to broadband internet, and therefore would not be able to bank online even if the service were available to them. Second, digital banking companies should increase their security so that users trust their products more. Hundreds of hacks against banks have led 1 in 3 Americans to say they don’t trust mobile banking.

Third, Help People Manage Past Banking Challenges — We need to change the credit checking system so we don’t continually penalize simple mistakes. Many new banks are working to create “second chance” bank accounts, which help people manage past banking challenges. When you apply to open a bank account, that bank will generate a ChexSystems Report that shows any bad practices you may have engaged in previously. If the bank decides you’re too risky based on that report, you’ll be denied due to your past financial troubles or poor credit history. However, many of those faults may have been made by mistake, or may be products of a broken system that failed you. A “second chance” bank account skips the ChexSystem report to give you an intermediate account. If we can increase access to these second chance accounts, we can help Americans build credit history and ultimately open standard accounts with more features.

When Rich Square, North Carolina lost its only bank in 2016, Lisa Evans felt the pain immediately. Her father had just died and she needed a loan to cover the funeral costs and to help jumpstart the family business that she now had to run. She didn’t know where to turn, since the town’s bank had been there for over 100 years. But as businesses failed along Main Street, Bank of Rich Square had to close. Lisa called every bank she could find, knowing that her $25,000 loan wouldn’t be approved via a digital banking service. After driving 17 miles past payday loan stores and check cashing stores, she eventually found a bank that would help her get her financial life back on track. Lisa thought about going into one of those payday lending stores, but she knew how the conversation would go — You’re approved for a loan. I’ll give you $300, and you give me back $1,500 in 1 month. Deal?